Whatever happened to the mother of all crashes that was supposed to arrive when the Federal Reserve began tightening its balance sheet back in 2022? For several years, I’ve been scratching my head, convinced that draining the balance sheet by trillions of dollars should have triggered a systemic banking failure or some other Black Swan event. In the past, crises like Lehman/AIG or the 2020 lockdowns took the blame, when in reality, the root cause was always monetary.

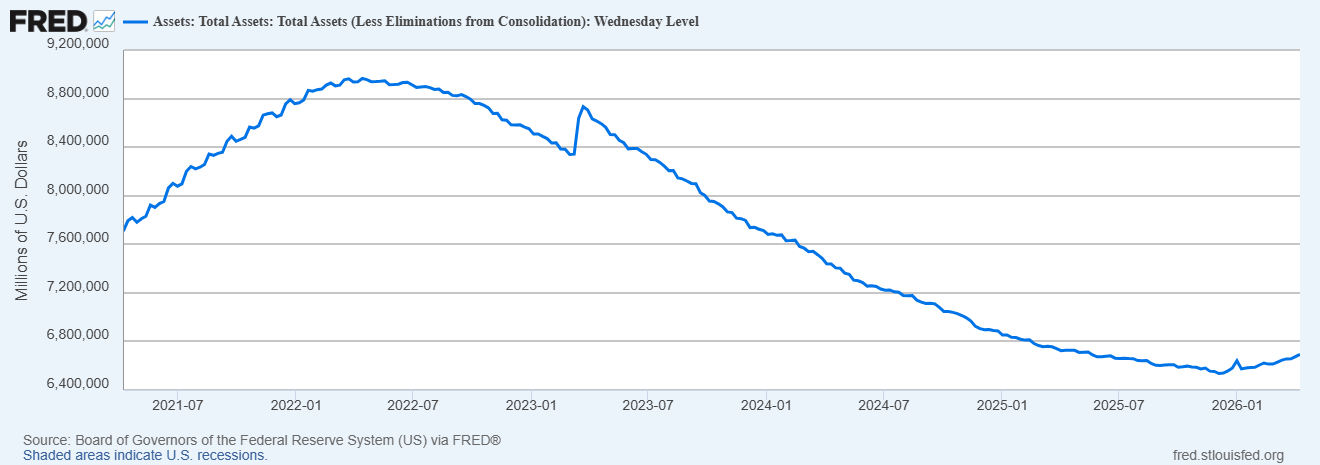

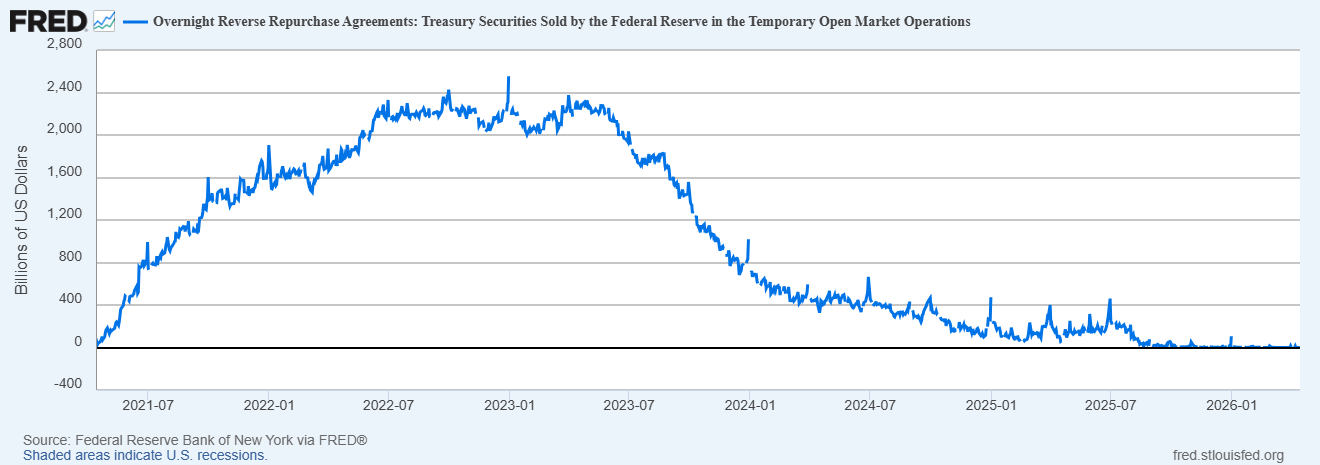

From the peak in June 2022 to the trough in December 2025, the asset side of the Fed’s balance sheet shrank by roughly $2.3 trillion. That was the front door. But through the back door, something else was happening on the liability side: the Fed’s Overnight Reverse Repo Facility (RRP) was releasing $2.5 trillion of previously frozen private liquidity back into the financial system.

If Quantitative Tightening (QT) removed liquidity, the RRP added it back... plus interest.

To recap: during QT, the Fed allows its holdings of Treasury securities and mortgage-backed securities (MBS) to mature. Financial intermediaries repay the Fed, and the Fed literally deletes that money from the system. This is the classic setup that exposes malinvestments, stresses credit markets, and reveals the imbalances described in Austrian Business Cycle Theory.

But this time it really was different because of the Reverse Repo Facility.

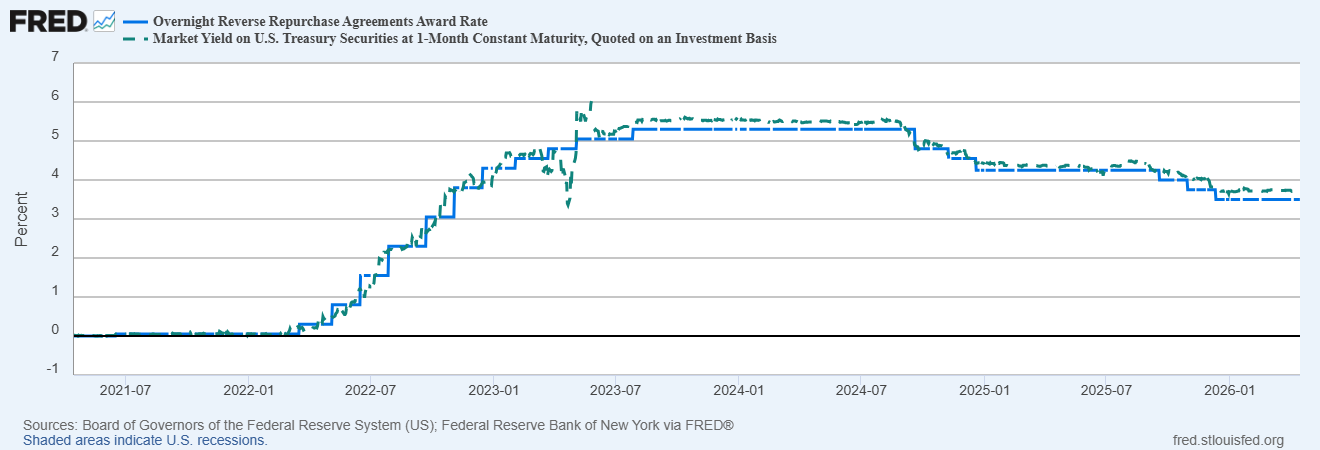

By mid-2023, the (March 2023) Silicon Valley Bank crisis had passed and the Fed’s Bank Term Funding Program was alive and well; then the hikes finally tapped out. Eventually, the 1-Month (4-Week) Market Yield on U.S. Treasuries outpaced the Fed’s RRP rate, and the incentive changed. Fund managers began a stampede out of the Fed’s facility and rotated into T-bills to chase a higher risk-free return.

In less than two years, the RRP withdrawals injected around $100 to $200 billion+ a month into the financial system at its peak. This was effectively a backdoor stimulus program that bypassed the Fed’s official QT narrative and funded the government’s deficit. Correlation does not equal causation, but it’s also not surprising that the Dow Jones broke out to new highs at almost the exact moment the RRP began to unwind.

The system was running on stored liquidity thanks to a giant buffer accumulated during the pandemic stimulus era. But as of 2026, that buffer is gone. The RRP liability has flatlined at essentially zero, meaning that the trillion-dollar offset to QT has been fully exhausted.

Perhaps it was no coincidence that once the RRP hit empty, the Fed’s tightening ended. On December 11, 2025, the Federal Reserve Bank of New York announced it would begin Reserve Management Purchases (RMP’s) at a pace of approximately $40 billion per month. While they use Fedspeak to avoid the term Quantitative Easing (QE), in reality, they’ve returned to official balance sheet expansion. They are being forced to replace the lost RRP liquidity with fresh money printing.

The math remains staggering. Since June 2022, the Fed was slashing its balance sheet by embarking on a QT narrative. The result? A net liquidity injection to the tune of $200 billion. And they called it “tightening.”

With the RRP buffer now empty, we are entering uncharted territory. The Fed’s $40 billion a month balance sheet expansion is several times less than what was entering the system via the RRP drain. Ironically, what the Fed hopes will act as QE might feel more like QT. We are about to find out just how long the system can survive a true monetary contraction.